LNG Tanker Glut Is Softening Blow for Consumers

[Stay on top of transportation news: Get TTNews in your inbox.]

Ships that carry liquefied natural gas are being built faster than new supplies of the fuel can come to market, helping to lower transport costs and cushioning consumers from paying even more for energy this winter.

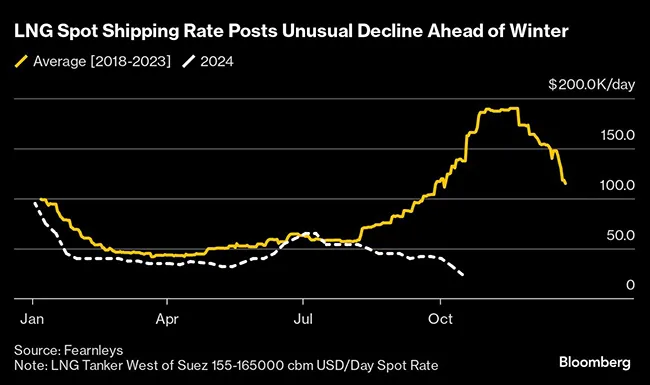

The cost of renting an LNG tanker on a short-term basis has fallen to the lowest for the time of year since at least 2018, data from shipbroker Fearnleys A/S shows. Shipping rates typically soar in the run-up to the heating season. Instead, they’ve been declining since August.

“Vessels are coming a little bit before the commodities do,” said Thomas Thorkildsen, chief commercial officer at shipowner Höegh Evi. “When you order a vessel in Korea or China, they are usually delivered on time, but often the production comes a bit late, so there is a mismatch.”

A shift in global trade patterns has also been a factor, with LNG tankers increasingly staying within either the Atlantic or Pacific regions, as they avoid Houthi militant attacks in the Red Sea. That means gas is being consumed closer to where it is produced, contributing to an excess of ships.

While the tanker glut reflects a temporary imbalance in the market, it’s good news for consumers. In Europe, gas prices are near the highest levels this year — even before the winter heating season gets under way — due in part to geopolitical conflicts in Ukraine, Russia and the Middle East.

Europe and Asia compete for a limited amount of global LNG supplies, and both regions have been relying on the fuel as a bridge from dirtier fossil fuels to renewables.

To serve this demand, new vessels have been coming to market at an increasing rate. A total of 36 tankers recorded their first loadings so far this year, compared to 30 in 2023, according to ship-tracking data compiled by Bloomberg. The order book for new-build tankers is also growing in anticipation of a further LNG supply boom by the end of the decade.

Meanwhile, some new supply keeps getting pushed back. The startup of the Golden Pass LNG export project in Texas, co-owned by QatarEnergy LNG and Exxon Mobil Corp., has been delayed until at least the end of 2025, following a contractor dispute.

Cheniere Energy Inc.’s Corpus Christi expansion plans to start producing LNG this year but will extend its ramp-up until the end of 2026. Sempra’s Costa Azul project in Mexico is now expected to begin commercial operations in 2026, a year later than initially targeted. Venture Global’s Plaquemines LNG project in Louisiana is still in commissioning, even though it’s due to start later this year.

As a result, spot shipping rates for the fourth quarter in both the Atlantic and Pacific basins have dropped below $50,000 a day for the first time in five years, according to data from Spark Commodities, based on assessments from LNG shipbrokers. The firm’s Atlantic freight rate is at $30,250 a day as of Oct. 17, the lowest yet for 2024.

Want more news? Listen to today's daily briefing above or go here for more info

That’s driven by “increased vessel availability and lower ton-miles as vessels stay within basin,” Spark CEO Tim Mendelssohn said, referring to a benchmark measurement for freight traffic.

Higher gas prices in Europe are also prompting more U.S. LNG to be delivered across the Atlantic. Meanwhile, Qatari LNG supplies to Europe have slumped, with more volume going to Asia, ship-tracking data show.

Longer term, as export projects catch up, the surplus is likely to evaporate, giving way to a tighter shipping market.

“The freight market should start to rebalance from 2026 as the expansion of global LNG export capacity accelerates,” analysts at Energy Aspects Ltd. said by email. But until then “the LNG freight market will remain relatively loose” as additional tankers outstrip the rate of new supply.